Weekly Market Outlook (07-11 October) | Forexlive

BIG EVENTS:

- Monday: Eurozone Exports. (China on holidays)

- Tuesday: Japan Income Summary, RBA Meeting Minutes, US NFIB Small Business Optimism Index.

- Wednesday: RBNZ Policy Decision, FOMC Meeting Minutes.

- Thursday: Japan PPI, ECB Meeting Minutes, US CPI, US Jobless Claims, New Zealand Manufacturing PMI.

- Friday: UK GDP, Canadian Labor Market report, US PPI, US University of Michigan Consumer Sentiment, BoC Business Outlook Survey.

Tuesday

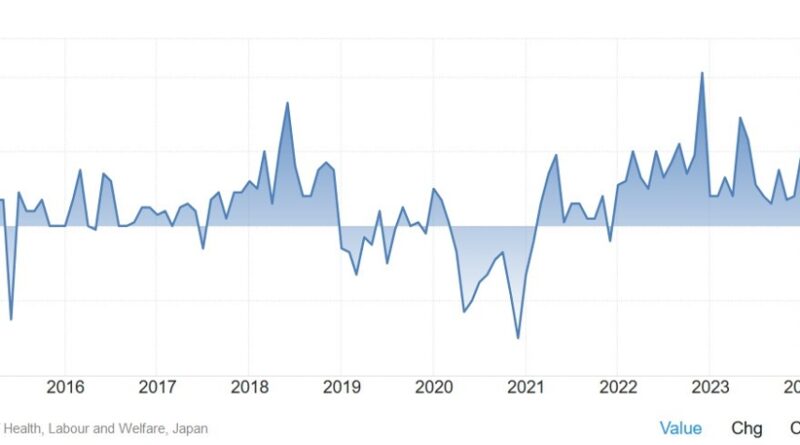

Japan’s Income Y/Y ratio is expected to be 3.1% vs. 3.6% before that. Wage growth has turned positive recently in Japan and is something the BoJ has always wanted to see in order to achieve its inflation target in a sustainable manner. The data should not change much for the central bank for now as they want to wait more to assess the development of prices and financial markets after the August action.

Japan’s Total Income YoY

Wednesday

The RBNZ is expected to cut the OCR by 50 bps and bring it to 4.75%. The reason for such expectations comes from the unemployment rate being at its highest level in 3 years, the main rate of inflation is within the expected range and the high frequency points that continue to show weakness. In addition, Governor Orr at the last press conference said that they considered several types of migration in the final decision of the policy and it includes a reduction of 50 bps.

RBNZ

Thursday

US CPI Y/Y is expected at 2.3% vs. 2.5% first, while the M/M figure is seen at 0.1% vs. 0.2% first. Core CPI Y/Y is expected at 3.2% vs. 3.2% before, while the M/M reading is seen at 0.2% vs. 0.3% first.

The final US labor market report came out better than expected and the market’s 50 bps gain in November quickly evaporated. The market is now finally in line with the Fed’s estimate of 50 bps of easing by the end of the year.

The Fed’s Waller said they could be quick to cut rates if labor market data worsens, or if inflation data continues to come in softer than everyone expected. He added that a new take on inflation could also prompt the Fed to halt its rate cuts.

Due to the latest NFP report, even if the CPI misses a bit, I don’t think they can think of a 50 bps decrease in November. That could be a talking point for the December meeting if inflation data continues to come in below expectations.

US Core CPI YoY

US Unemployment Reports continue to be one of the most important releases to follow each week as they are a timely indicator of the state of the labor market.

Early Claims are still in the 200K-260K range made since 2022, while Continuing Claims after rising steadily over the summer have improved significantly in recent weeks.

This week First Reports are expected at 230K vs. 225K before that, there is no agreement for Continuous Reports at the time of writing although the first release showed a decrease to 1826K.

US Unemployment Claims

Friday

The Canadian Labor Market Report is expected to show 28K jobs added in September vs. 22.1K in August and Unemployment Rate increases to 6.7% vs. 6.6% before that. The market is pricing in an 83% chance of a 25 bps cut in the next session but as inflation continues to surprisingly lower, a weak report may raise the chances of a 50 bps cut bps.

Unemployment Rate in Canada

US PPI Y/Y is expected at 1.6% vs. 1.7% first, while the M/M numbers are seen at 0.1% vs. 0.2% first. Core PPI Y/Y is expected at 2.7% vs. 2.4% before, while the M/M reading is seen at 0.2% vs. 0.3% first.

Also, the data is unlikely to make the Fed argue about a 50 bps cut at the November meeting even if it is wrong. The risk now is that inflation will remain at a high level or even shock upwards.

US Core PPI YOY

#Weekly #Market #Outlook #October #Forexlive